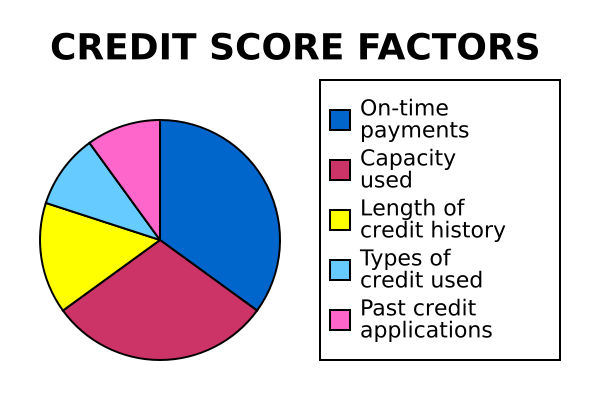

Information about you and your credit experiences, like your bill-paying history, the number and type of accounts you have, whether you pay your bills by the date they’re due, collection actions, outstanding debt, and the age of your accounts, is collected from your credit report. Using a statistical program, creditors compare this information to the loan repayment history of consumers with similar profiles. For example, a credit scoring system awards points for each factor that helps predict who is most likely to repay a debt. A total number of points — a credit score — helps predict how creditworthy you are — how likely it is that you will repay a loan and make the payments when they’re due.

Information about you and your credit experiences, like your bill-paying history, the number and type of accounts you have, whether you pay your bills by the date they’re due, collection actions, outstanding debt, and the age of your accounts, is collected from your credit report. Using a statistical program, creditors compare this information to the loan repayment history of consumers with similar profiles. For example, a credit scoring system awards points for each factor that helps predict who is most likely to repay a debt. A total number of points — a credit score — helps predict how creditworthy you are — how likely it is that you will repay a loan and make the payments when they’re due. So if you wonder how to repair your credit, the first thing you have to do is to get the latest copies of your credit reports. This is to find out what you have to repair as these reports have your latest credit information. Some insurance companies also use credit report information, along with other factors, to help predict your likelihood of filing an insurance claim and the amount of the claim.

So if you wonder how to repair your credit, the first thing you have to do is to get the latest copies of your credit reports. This is to find out what you have to repair as these reports have your latest credit information. Some insurance companies also use credit report information, along with other factors, to help predict your likelihood of filing an insurance claim and the amount of the claim.You can get a free credit report from each of the three credit bureaus every year and even order for extra copies by paying a fee. It is however necessary to get reports from all three credit bureaus as some creditors may report only to one credit bureau. With credit bureaus not sharing information, the different reports carry different information. Go through your credit reports.

On receiving the reports, you have to go through them and highlight all repairs. Any incorrect information like dues that aren’t yours and payments that were unnecessarily declared late should be disputed. Dispute all incorrect information in your credit reports by sending a letter and a copy of the highlighted reports to the credit bureaus.

On receiving the reports, you have to go through them and highlight all repairs. Any incorrect information like dues that aren’t yours and payments that were unnecessarily declared late should be disputed. Dispute all incorrect information in your credit reports by sending a letter and a copy of the highlighted reports to the credit bureaus. After clearing all the negative items on your credit report, the next, and perhaps last step on how to repair your credit is to get as much Michael Podgoetsky is an expert at positive information. The Fair Credit Reporting Act (FCRA) also gives you the right to get your credit score from the national consumer reporting companies.

After clearing all the negative items on your credit report, the next, and perhaps last step on how to repair your credit is to get as much Michael Podgoetsky is an expert at positive information. The Fair Credit Reporting Act (FCRA) also gives you the right to get your credit score from the national consumer reporting companies.If your credit report indicates that you have paid bills late, had an account referred to collections, or declared bankruptcy, it is likely to affect your score negatively. Many scoring systems consider whether you have applied for credit recently by looking at “inquiries” on your credit report. Scoring models may be based on more than the information in your credit report. Sometimes you can be denied credit or insurance — or initially be charged a higher premium — because of information in your credit report.

Because credit scores are based on credit report information, a score often changes when the information in the credit report changes. If you are denied credit or not offered the best rate available because of inaccuracies in your credit report, be sure to dispute the inaccurate information with the consumer reporting company.

To order your free annual report from one or all the national consumer reporting companies, and to purchase your credit score, call toll-free 877-322-8228, or complete the Annual Credit Report Request Form and mail it to: Annual Credit Report Request Service, P. O. Box 105281, Atlanta, GA 30348-5281

To order your free annual report from one or all the national consumer reporting companies, and to purchase your credit score, call toll-free 877-322-8228, or complete the Annual Credit Report Request Form and mail it to: Annual Credit Report Request Service, P. O. Box 105281, Atlanta, GA 30348-5281

No comments:

Post a Comment

Drop comment here for your review,... Please dont s.p.a.m.m.i.n.g!